1a. Explain the relationship in the short run between the marginal costs of a firm and its average total costs.

Average cost is the sum of total fixed cost and total variable cost. Total fixed costs are costs that stay constant throughout, for example paying rent of the factory. Total variable costs are costs that change constantly according to the activity, for example labor and material costs.

Marginal cost, is the cost in total it takes to increase one additional unit of production. Since it the sum of total average cost, and the cost of the additional unit, marginal cost is affected by the behavior of the variable cost. Since fixed cost is always constant, it would not affect the marginal cost.

1b. Define the law of diminishing returs and assess the likelihood that it will be experienced by a firm producing a product in a consumer good market.

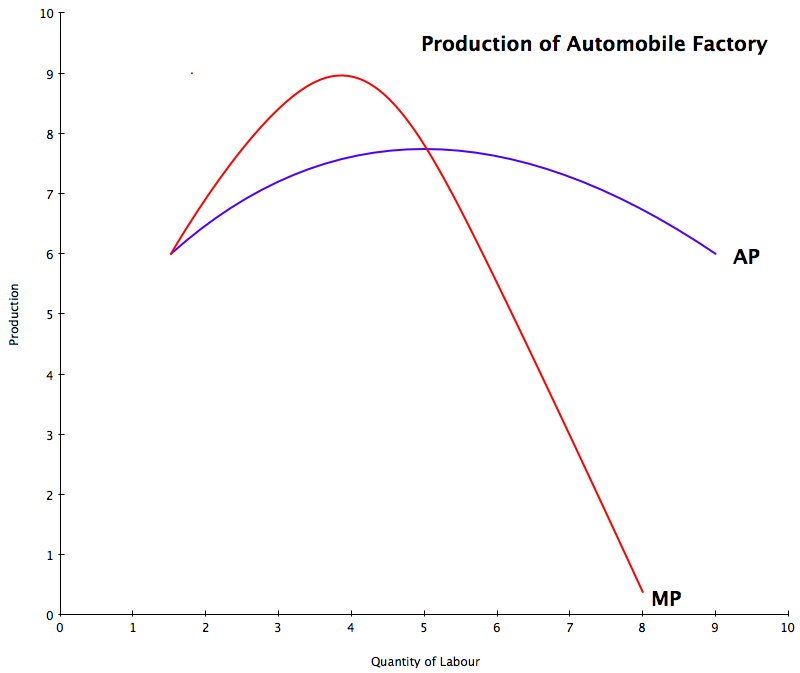

When increasing variable resource with an fixed resource, at one point the marginal production starts to decrease. For example an small automobile factory has 3 workshops that can be used by technical experts to build cars. With 3 people workers, the production keeps rising. With 4 workers, it still keeps rising expecting that he/she can be doing odd jobs (providing coffee, cleaning up areas, etc). However from the 5th worker, production starts decreasing. This is because if there are 5 workers, the small factory is too packed workers start getting in each others way. Therefor increase in variable resource for more than 4 workers will cause the factory to start experiencing law of diminishing returns in this case.